We’ve narrowly avoided a second labor strike at 36 U.S. East and Gulf Coast ports. The tentative agreement struck between the International Longshoremen’s Association (ILA) and the United States Maritime Alliance (USMX) after the 3-day strike in October was set to expire on January 15. With this deadline rapidly approaching, concerns over another potential strike are escalating. An agreement was reached on January 8th, but ratification from the ILA union members is still needed before it is finalized.

Avoiding a strike is critical to global supply chains and economies, with an estimated cost of $5 billion per day of strikes and the East and Gulf Coasts being critical components of supply chains for numerous industries.

Impacts from the 3-day strike in October

When the two sides failed to reach an agreement by the previous September 30 deadline, ILA workers went on strike, effectively shutting down operations at 36 major U.S. ports. The October strike led to several notable disruptions:

- Increased Berthing Time: Vessels faced longer wait times to dock.

- Extended Container Dwell Times: Both imports and exports experienced delays at affected ports.

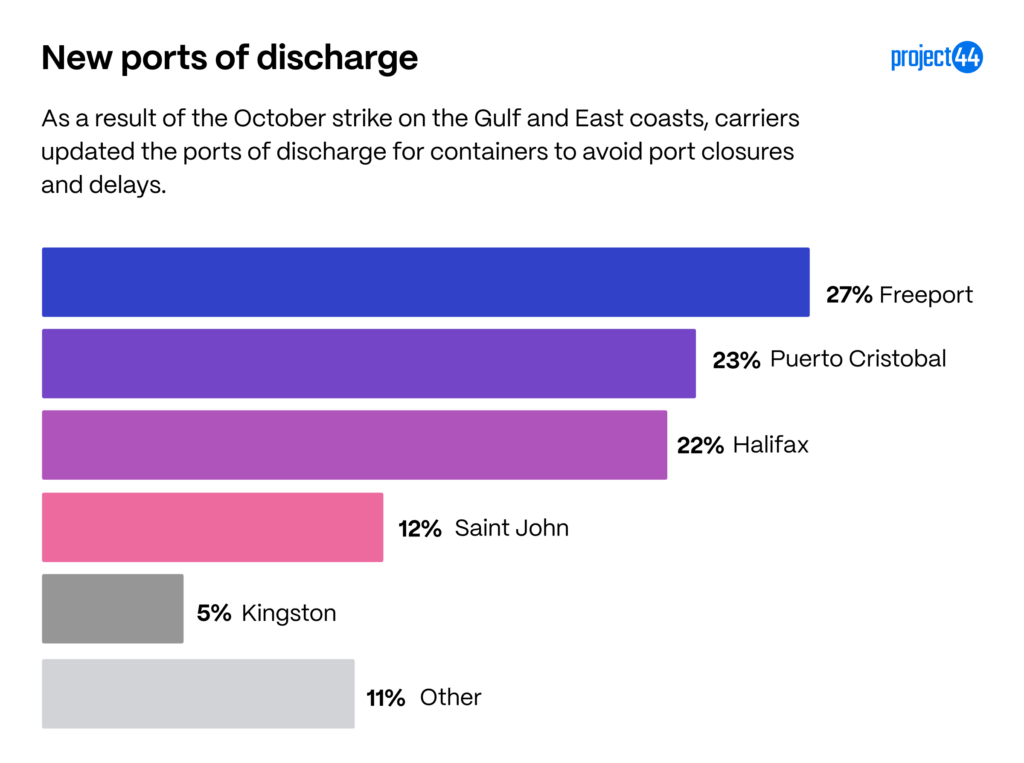

- Diversions to Alternative Ports: Containers were rerouted to unimpacted ports, primarily in the Bahamas, Latin America, and Canada.

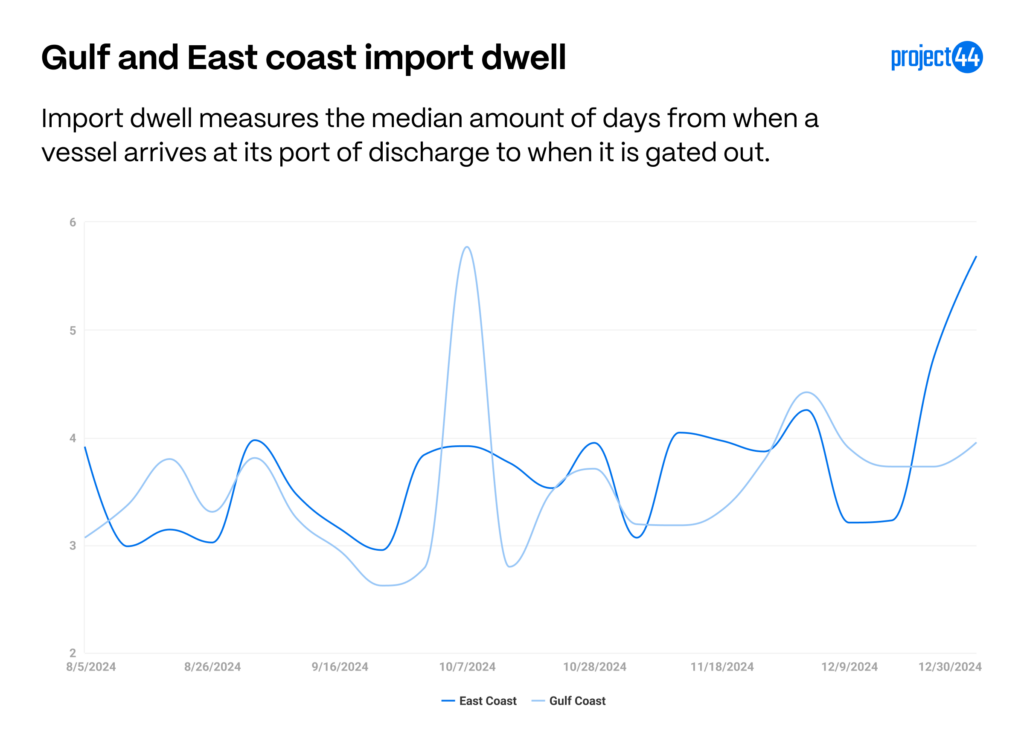

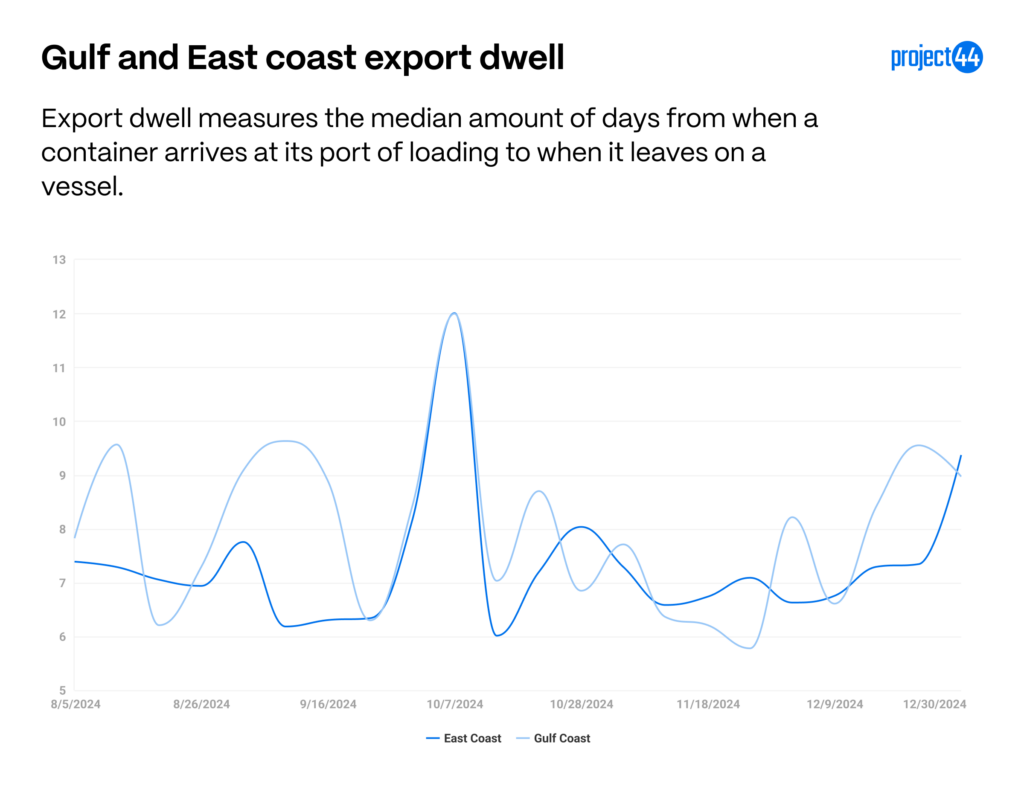

Container dwell time

During the 3-day strike, container dwell times saw minimal disruption, with only one week experiencing a major spike.

Import dwell primarily spiked at Gulf Coast ports, while East Coast ports were largely unaffected.

Export dwell impacted both coasts similarly but returned to normal levels quickly.

The recent rise in dwell times for both imports and exports is attributed to holiday-related port closures.

Rerouted containers

To maintain vessel circulation during the strike, carriers diverted containers to alternative ports, minimizing interruptions to vessel schedules and avoiding extended berthing delays at closed ports.

Most susceptible industries

Another strike would have serious consequences for global supply chains, with an estimated cost of $5 billion per day. The East Coast ports handle approximately 35-40% of U.S. imports and exports, while the Gulf Coast ports account for 10-15% of imports and 20-25% of exports. These percentages reflect overall trade volumes, but certain industries would be disproportionately affected. Below is a breakdown of major imports and exports by region.

Gulf Coast Ports:

Energy and Petrochemicals:

Gulf Coast ports, especially Houston and New Orleans, handle 60-70% of the U.S. exports of crude oil, refined petroleum products, and natural gas.

A significant portion of the petrochemical supply chain, including plastics and chemical feedstocks, also moves through these ports.

Agriculture:

About 60% of U.S. grain and soybean exports flow through Gulf Coast ports, with New Orleans being a major hub for agriculture exports from the Midwest.

Heavy Manufacturing & Machinery:

Gulf Coast ports handle around 25-30% of U.S. exports of industrial machinery and heavy equipment, much of it bound for Latin America and Europe.

East Coast Ports:

Retail and Consumer Goods:

East Coast ports manage 35-40% of U.S. consumer goods imports such as electronics, clothing, and furniture. Ports like New York/New Jersey and Savannah are critical for trade with Europe and Asia.

Many of these imports are destined for the East Coast and Midwest retail markets.

Automotive Industry:

Approximately 30-35% of U.S. automotive imports and exports pass through East Coast ports, especially vehicles and parts from Europe. The Port of Baltimore is a key hub for RoRo (Roll-on/Roll-off) vessels. When the port temporarily halted operations, the industry remained stable by rerouting shipments to nearby ports. However, if a strike occurs in January, disruptions to manufacturing will likely be unavoidable.

Pharmaceuticals and Chemicals:

Approximately 30-35% of U.S. pharmaceutical imports flow through East Coast ports. This includes active pharmaceutical ingredients (APIs) and finished drugs from Europe, India, and other regions.

Food and Beverages:

East Coast ports manage 30-40% of U.S. food and beverage imports, including perishables like produce, seafood, and processed foods from Europe and Africa.

Industries affected by both coasts:

Construction Materials:

Combined, the East and Gulf Coast ports handle about 25-30% of U.S. imports of steel, cement, and other construction materials, primarily sourced from Europe and Latin America.

Tentative agreement

Terms of the agreement reached on January 8th have not been made public at this time, but the key issue stopping the contract from moving forward prior to this point hinged on port automations. The USMX would like to enable more automation among ports, but the ILA argues that this will be removing jobs. While it is uncertain what middle ground was reached, it likely has something to do with the issue of automation.

If this agreement is ratified, the East, Gulf, and West coast ports in the United States will have stable contracts until 2028, when the West coast contract expires, removing labor uncertainty in the U.S. as a major supply chain concern.

Summary

The impending January 15th deadline for contract negotiations between the ILA and USMX has raised fears of another port strike, which could severely disrupt U.S. supply chains. An agreement was reached on January 8th but is still pending ratification from the union members. The October strike highlighted the vulnerabilities of key industries, causing increased berthing times, container dwell delays, and rerouting to unimpacted ports. While East Coast ports handle significant consumer goods, automotive, and pharmaceutical imports, Gulf Coast ports are critical for energy, agriculture, and heavy manufacturing exports. The economic stakes are high, with potential daily losses reaching $5 billion, underscoring the urgency for a resolution.